Mobile Home Insurance: 5 Essential Tips for Better Coverage

Article Summary

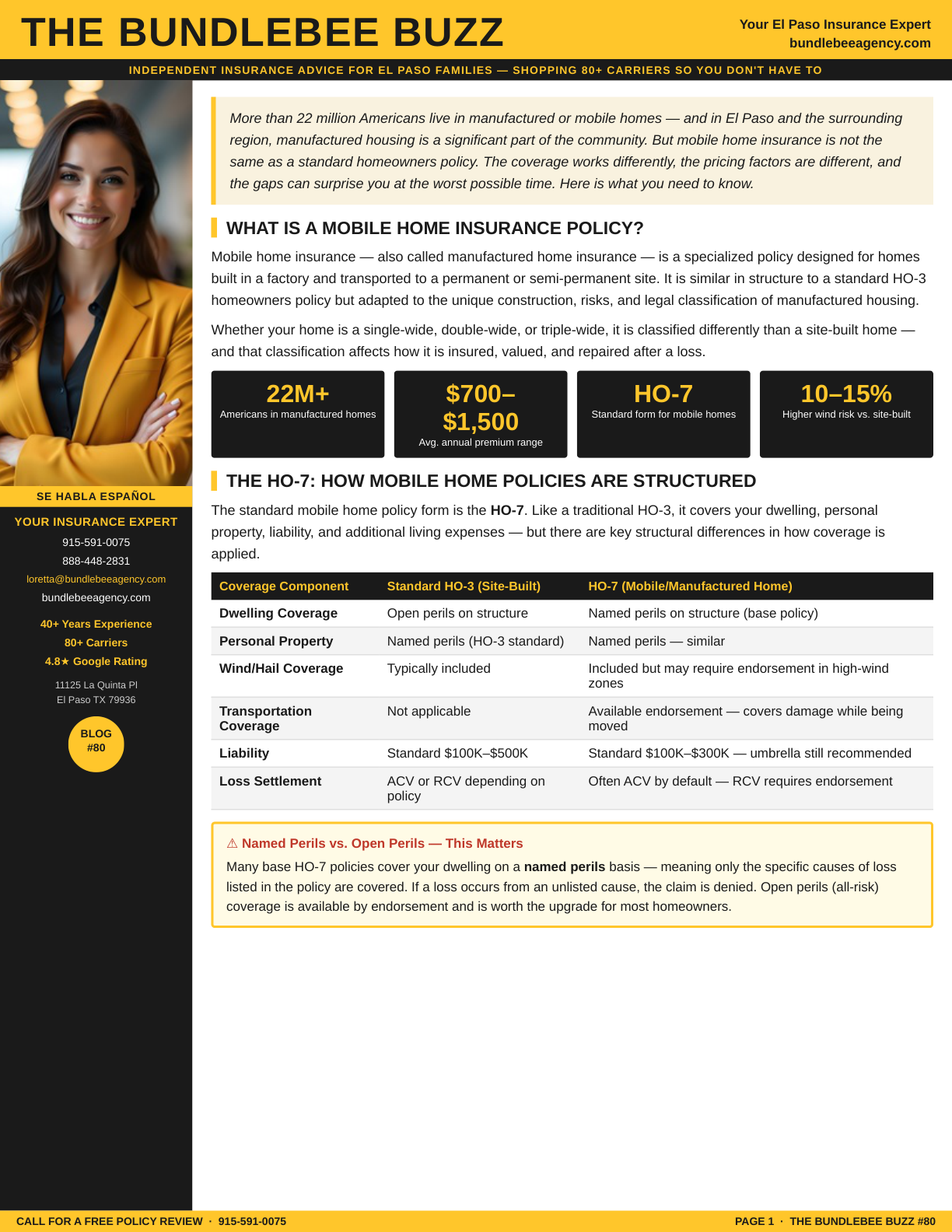

Mobile home insurance is crucial for protecting your manufactured home, yet many homeowners are unaware of its unique features. Unlike standard homeowners policies, mobile home insurance, also known as manufactured home insurance, is specifically designed for homes built in factories and transported to a permanent site. This type of insurance covers various aspects, including dwelling, personal property, liability, and additional living expenses, but it comes with its own set of challenges. For instance, mobile home policies often operate on a named perils basis, meaning only specific causes of loss are covered unless you opt for an open perils endorsement. Additionally, factors such as the age of the home, compliance with HUD standards, and the anchoring system can significantly impact your premiums. Understanding these elements can help you avoid costly gaps in coverage. In this blog, we’ll explore five essential tips to ensure you have the right mobile home insurance policy tailored to your needs.

Need help reviewing your coverage? Contact BundleBee Insurance Agency for a free policy review.

Why Mobile Home Insurance Is Different

Mobile home insurance differs from standard homeowners insurance because manufactured homes face unique risks. Transportation, anchoring systems, skirting, and HUD compliance standards can all affect coverage eligibility and claim outcomes. Many policies are written on a named-perils basis, meaning only specifically listed causes of loss are covered unless additional endorsements are purchased. Understanding these differences can help homeowners avoid surprises after a claim.

Common Mobile Home Insurance Coverages

Most mobile home insurance policies include dwelling coverage, personal property coverage, liability protection, and loss-of-use coverage. Dwelling coverage helps repair or rebuild the structure after a covered loss. Personal property coverage protects belongings such as furniture, electronics, and clothing. Liability coverage can help if someone is injured on your property, while loss-of-use coverage may help pay for temporary living expenses if the home becomes uninhabitable due to a covered claim.

Common Risks Mobile Homeowners Face

Mobile homes may be more vulnerable to windstorms, hail, fire, water damage, and theft than traditional homes. Older manufactured homes can also face coverage restrictions due to age, condition, or outdated electrical and plumbing systems. Reviewing your policy regularly helps ensure your coverage limits remain adequate and that any endorsements needed for your specific situation are included.

Tips for Choosing the Right Policy

Before purchasing a policy, compare replacement cost options, deductible choices, liability limits, and available endorsements. Ask whether the policy provides replacement cost or actual cash value settlement for both the structure and personal property. Homeowners should also verify whether detached structures, carports, sheds, and porches are covered.

Related Resources

- Learn about wind and hail deductibles and how they affect claim payouts.

- Understand the difference between replacement cost and actual cash value coverage.

- Review common homeowners insurance exclusions that may leave coverage gaps.