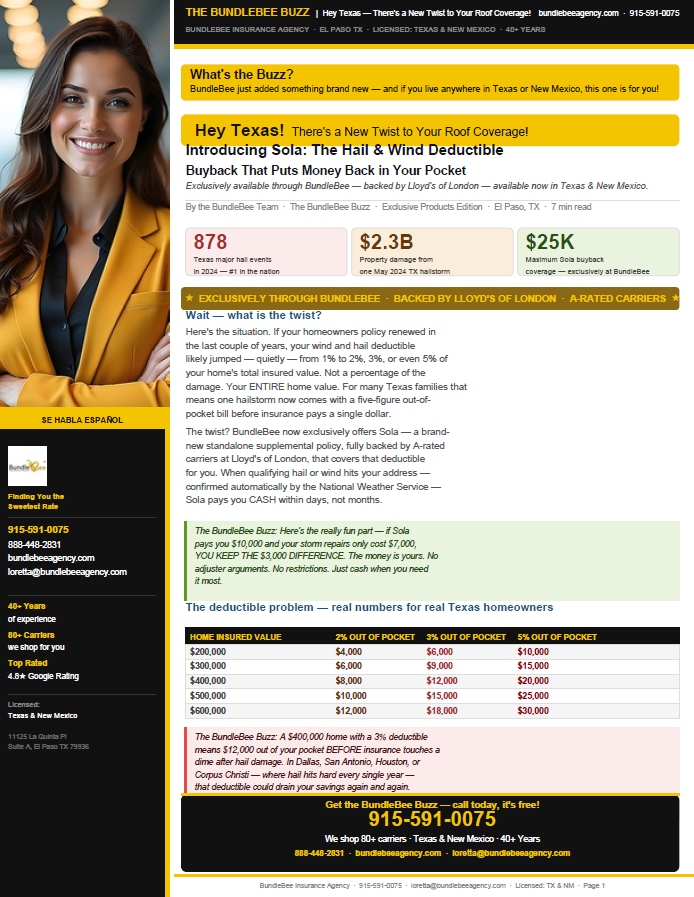

Wind and Hail Deductible Buyback: 7 Powerful Ways to Protect Your Savings: Article Summary

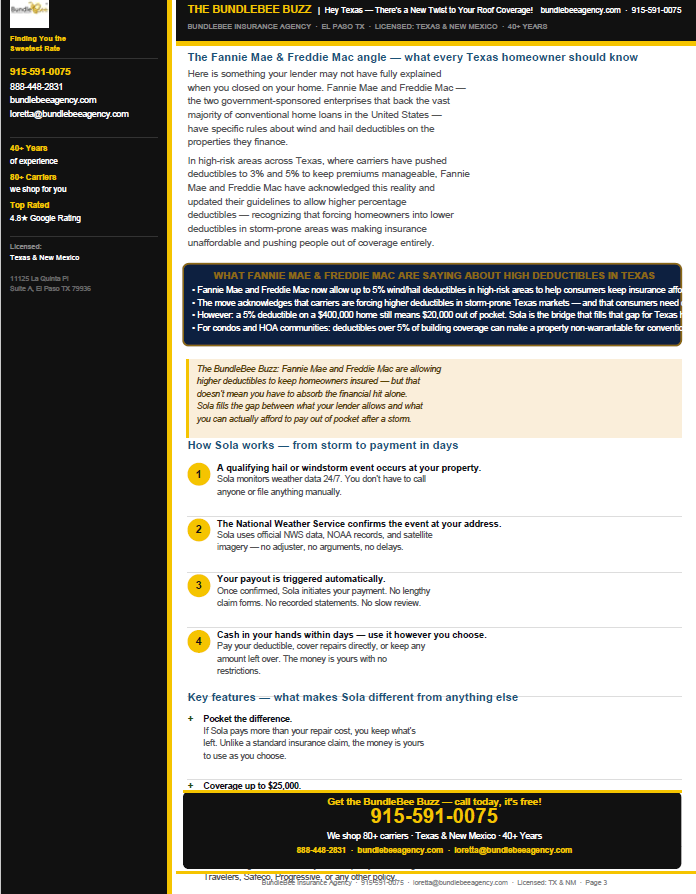

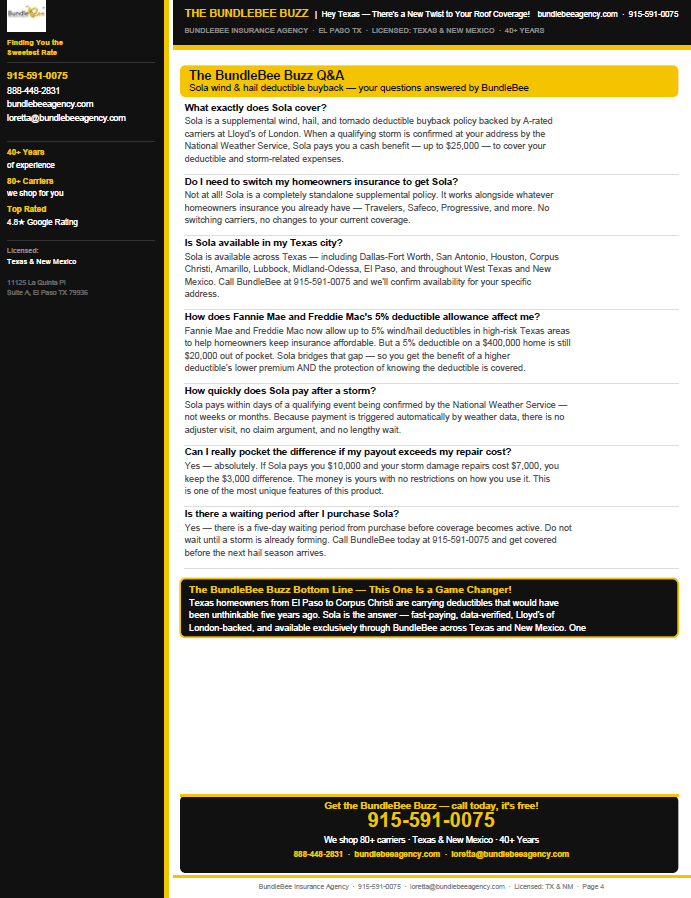

Wind and hail deductible buyback coverage is becoming increasingly important for Texas homeowners as insurance carriers continue raising percentage-based deductibles to keep premiums affordable. Many homeowners are surprised to learn that a 2%, 3%, or even 5% wind and hail deductible applies to their home’s insured value rather than the amount of damage sustained. For a $400,000 home, that could mean paying anywhere from $8,000 to $20,000 out of pocket before insurance contributes a single dollar toward repairs. As severe weather events continue affecting communities across Texas, these higher deductibles can create significant financial strain for homeowners who are unprepared for a major storm.

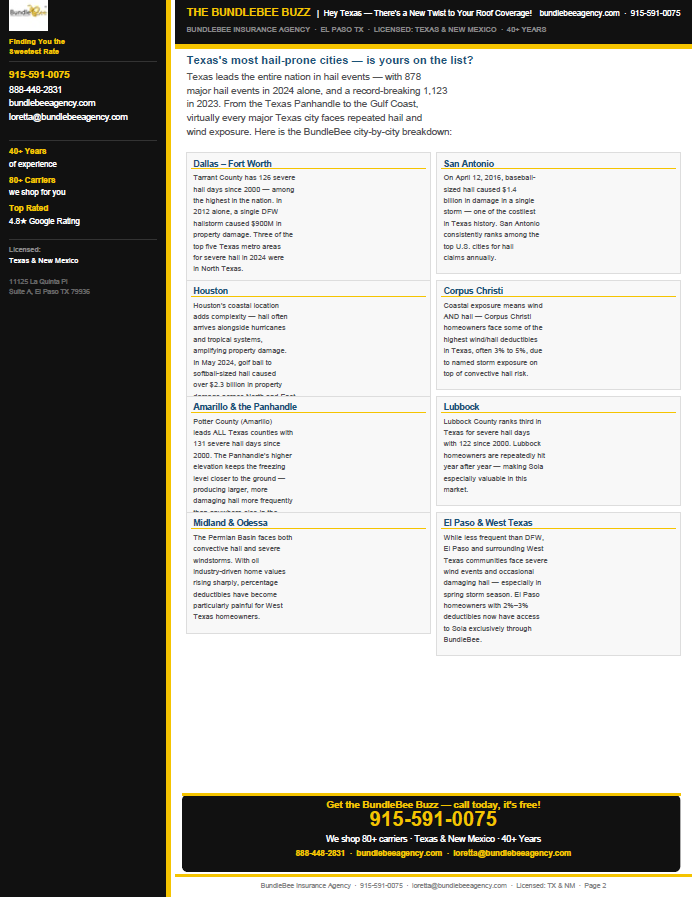

This guide explains how wind and hail deductible buyback coverage works, why percentage deductibles have become more common, and how supplemental protection can help reduce financial exposure after a qualifying storm. You’ll learn how deductible buyback programs function, the role of weather verification systems, common deductible amounts faced by Texas homeowners, and why cities such as Dallas-Fort Worth, Houston, San Antonio, Lubbock, Midland-Odessa, Corpus Christi, Amarillo, and El Paso face elevated hail and wind risks. We also discuss Fannie Mae and Freddie Mac deductible guidelines, the impact of rising storm losses on insurance policies, and practical strategies homeowners can use to better protect their finances. Whether you own a home in a high-risk hail region or simply want greater peace of mind during storm season, understanding wind and hail deductible buyback coverage can help you prepare for unexpected weather-related expenses.